The Impact From Lower Cost Carriers - American to Discontinue Boston-San Francisco Route

After operating the Boston (BOS) to San Francisco (SFO) route non-stop since 1998, American Airlines (AMR) recently announced it will discontinue their twice daily round-trips between BOS and SFO effective this November.

This analytical report uses the most recent publicly available data to show the competitive landscape for the BOS-SFO route for year 2009 and Q1 2010. Note: some 2010 data is not yet available.

Before reviewing the recent data, it’s worth noting some past history for the BOS-SFO market:

From 1998 to 2009, United (UAUA) and American were virtually (see note) the only two airlines with non-stop flights between BOS & SFO. Note: In 2004 and 2005, America West and Delta (DAL) briefly operated flights in the BOS-SFO market. JetBlue (JBLU) started seasonal service in 2007.

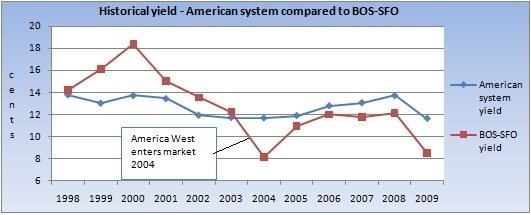

During the time American and United were the only two airlines in the BOS-SFO non-stop market, passenger yields were at or above overall system yields.

In February 2009, Virgin America entered the BOS-SFO market. In May 2009, JetBlue went from seasonal to daily full year service.

Available seats (monthly) in the BOS to SFO market increased by over 60% as they went from just over 30,000 at the beginning of 2009 to over 53,000 in August.

During year 2009, American and JetBlue’s available seats between BOS and SFO remained mostly stable while United and Virgin America increased capacity significantly. Throughout the year, United claimed approximately 50% of the available seats. Starting in 2010, when compared to 2009, JetBlue has nearly doubled the available seats in the BOS-SFO market.

In spite of the significant increase in capacity by Virgin America and JetBlue, American and United maintained the highest load factors for most of the year in the BOS to SFO market. Further, United and American’s summer load factors in this market were significantly higher than their overall system load factors for the same time period.

It would be logical to expect the added capacity from Virgin America and JetBlue, both of which are lower cost carriers, would drive fare yields lower. This in fact did occur as the average fare in the second quarter dropped significantly from the first quarter when United and American were primarily the only two carriers operating this route.

However, after the average fare fell by 14% from Q1 to Q2, even with the significant increase in added seats, the Q3 average fare increased by 10%. This fare increase was likely caused by seasonal demand and further pushed by an overall industry increase in fares. Note: Q1 2010 fares are not yet available.

All airlines reconcile route segment revenue with segment costs. Any airline will or should attempt to garner the highest profits possible. To achieve higher profits, airlines frequently move aircraft to markets that may provide higher yields and more (potential) profit.

While load factors in this specific market were relatively high, excluding Virgin America, passenger yields were considerably less than each airlines system yield.

For year 2009, American had the highest (negative) differential between their system passenger yield and the average yields in the Boston to San Francisco market.

Through the later 90’s into the early 2000’s, BOS-SFO yields relative to other markets were very high. When looking at the historical impact of lower cost competitors into the BOS-SFO market, the drop in average passenger yields has been significant. Using Q2 data from 1998 thru 2003, BOS-SFO yields were consistently higher than American’s system yields. In 2004 when lower cost carrier America West entered the market, BOS-SFO yields dropped by over 30%.

Since 2004 BOS-SFO average Q2 yields have remained consistently less than American’s system yields. As more detailed above, in year 2009, the BOS-SFO yield (negative) differential for American increased substantially as available capacity nearly doubled. Note: American typically has at or near the industry’s highest passenger system yields.

Conclusion- the BOS to SFO market has seen the available seat capacity nearly double from what it was in early 2009. For year 2010, JetBlue is adding significant capacity to/from BOS. This market “saturation” drives fares lower, especially over the winter months when passenger demand typically drops.

Accepting there may be other reasons beyond the data provided in this analysis, it appears the reason for American pulling out of the BOS-SFO market may be because there are other higher yield markets to operate the equipment that has been used on the BOS-SFO segment.

Data sources: SEC, BTS, and DOT

Virgin America does not file SEC filings. As such some data may not be available.

Internal company data may be different from what is provided in this report. Any errors are unintentional.

{kind=link}

No comments:

Post a Comment