A Refutation of the Arguments Against the United-Continental Merger

by Davide Pavone June 20, 2010 }

The merger between United Airlines (UAUA) and Continental Airlines (CAL) has generated lively debate amongst analysts, politicians, and business leaders. This article refutes the more common arguments against the horizontal agreement.

Mergers do not work.

Given that their own success, as well as the future of the firm, is at stake, it is vital that United and Continental managers correctly assess the benefits and costs of the horizontal agreement. The assessment is inherently subjective, and does not simply include cost calculations and revenue projections.

Successful business arrangements are akin to successful marriages; they work efficiently, but only the parties involved are aware of the relative costs and benefits. Moreover, like a marriage, the agreement’s success depends more on a tacit understanding than objective cost-benefit calculations. A regulatory agency is not in a position to accurately estimate the benefits and costs of any horizontal merger.

It is not possible for regulators to apply the rule of reason as they lack the required information. Regulators assume the existence of the information they require to decide a case. The necessary information is embedded in future economic activity, becomes available once the future economy activity has occurred, and is apparent only to the concerned economic agents. It is fallacious to state ex ante that the costs of a merger are greater than its benefits, or the merger will be unsuccessful. Given that the knowledge of future prices is required to determine whether a merger will be profitable, the success of a merger is only determined ex post.

The merger would reduce service and jobs.

The question to ask is not how a reduction in air service and jobs may be prevented, but whether factors of production are being allocated efficiently. If it is not possible for the post-merger United to earn its cost of capital on a particular route, the route should be terminated. If United continues to operate the route, the use of factors of production is wasteful. By eliminating unprofitable air service and jobs, United allows scarce factors of production to be used (more) profitably.

The post-merger airline would have a considerable market share and significant market power.

In order to discuss United’s post-merger market share, it is necessary to first define the relevant market. Unfortunately for merger opponents, it is not possible to define the relevant market in a non-arbitrary fashion.

Suppose we wish to determine United’s post-merger market share. Should the relevant market be defined nationally, or divided into regional submarkets? If the latter approach is chosen, do we simply examine flights between two specific airports (e.g. LAX and ORD), or two general areas (e.g. the LA basin and Chicago)? Do we assume that all passengers are homogeneous, or take differences into account (e.g. business traveler as opposed to leisure traveler)? How are these questions to be answered unambiguously?

For the sake of argument, let us assume that it is possible to determine the post-merger airline’s market share in a non-arbitrary manner. Despite this achievement, the number would be meaningless as economic theory does not provide a threshold above which a firm may earn economic profit in the long-run.

It is fallacious to state that a firm with a market share of (say) 33.3% has sufficient market power to earn economic profit in the long-run. Likewise, it is erroneous to conclude that market output will fall, and the market price will rise, due to a horizontal agreement which raises the Herfindahl index of market concentration by (say) 175 points. The thresholds are completely arbitrary and have no scientific value. But, what if the merger does permit the airline industry to raise air fares?

Contrary to what certain political and business leaders may think, a rise in airline ticket prices would not indicate market power. In order for the higher price to be “monopolistically-competitive”, the lower price must have been “competitive.” However, how do we know that the lower price was indeed a competitive price? We do not know.

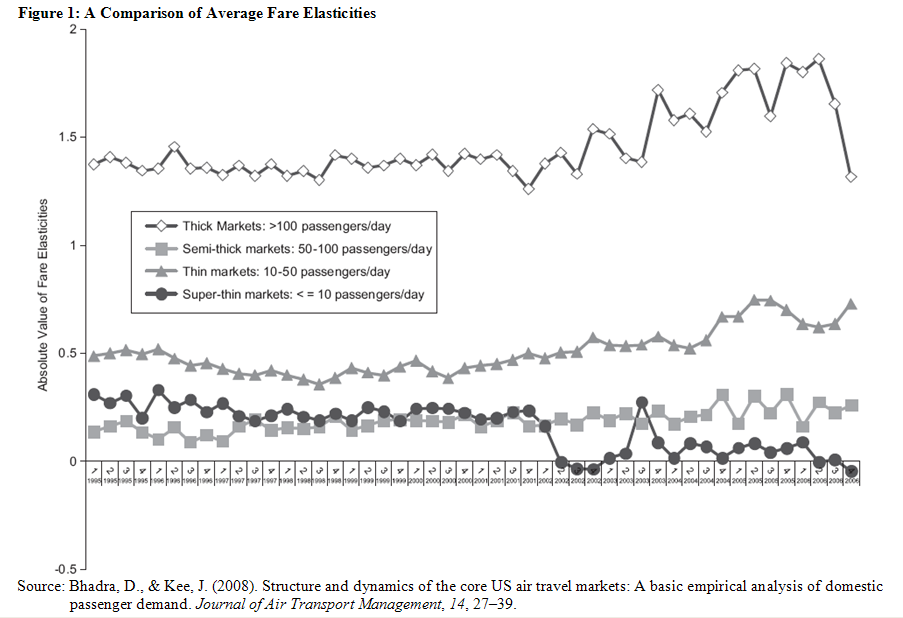

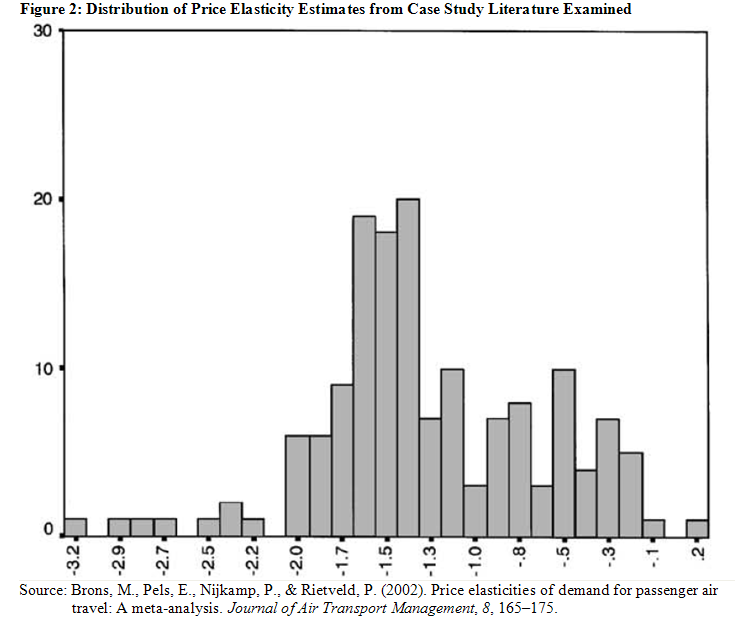

Given that a clearly established competitive price does not exist, it would be incorrect to declare that the higher prices are monopolistically-competitive. In fact, it could be argued that prices rose from a “sub-competitive” level to one that is “competitive.” Moreover, merger opponents fail to realize that the demand for air travel is (generally) elastic.

It is generally difficult for an airline to obtain market power because the demand curve for air travel, as it presents itself to each airline, is elastic (click on charts to enlarge). In other words, the percentage change in quantity demanded is greater than the percentage change in price. As a result, the market power argument against the merger is not relevant.

Conclusion

The arguments put forward by merger opponents are not supported by economic theory. Regulators are not in a position to evaluate the advantages and disadvantages of the merger. Moreover, contrary to the prevailing attitude, it is only possible to determine the success of the merger ex post. Lastly, the arguments concerning a reduction in output, loss of jobs, and creation of market power are not relevant to the debate.

Disclosure: The author holds no positions with regards to UAUA and CAL.

About the author: Davide Pavone

Davide Pavone is an undergraduate student enrolled in the Desautels Faculty of Management (McGill University). He is pursuing a Bachelor of Commerce, and his main and secondary fields of study are finance and economics respectively.

{kind=link}

{kind=link}

No comments:

Post a Comment